The numbers don’t lie: 33 years of Australian superannuation

I moved to Australia as both a young man and an economic refugee.

Having graduated university right as the Great Recession (AKA US subprime mortgages) rendered my career prospects in New Zealand pretty much zero, I took my place among the tens of thousands of Kiwis crossing the ditch.

I found exactly what the record numbers in 2026 making the same journey are finding:

A superior economic reality in a culture only marginally different from back home; opportunities to work your way up in, and out into, the world; and a genuine path toward building wealth.

What I also found, and completely neglected to understand until many years later, was that as soon as I started my first full-time job, I also became an investor.

Since 1992, superannuation has been compulsory in Australia.

I didn't choose it. I didn't understand it. Nobody sat me down and asked if I wanted to become an investor — it just happened, automatically, with my first payslip, at a rate I didn't notice and couldn't have changed even if I had.

That's true for every working Australian resident. You don't opt in. You don't opt out. If you’re earning, you’re investing.

So in this week’s Benchmark, I’m sharing and breaking down 15 remarkable numbers from Australia’s 33 year compulsory super story.

Some are impressive. Some are uncomfortable. All are worth thinking about.

1. Super now takes 300% more of your pay than it did in 1992

The compulsory cut of every payslip is up from 3% in 1992 to 12% today. No opt-outs. The UK's auto-enrolment lets workers leave. The US has no general compulsory retirement savings at all. Australia's version is rare by design: automatic, non-negotiable, and untouched by 33 years of politics.

2. Employers poured $156.3 billion into super in the year to December 2025

That’s more than Australia's entire defence budget. Or roughly what the whole ASX 200 pays in company tax, combined. It arrives whether the economy is booming or bracing for recession.

3. $457 million flows into super every single day

That’s $3.2 billion a week, rain or shine, recession or boom. The number barely moves regardless of what's happening in the economy that generates it.

4. The total super pool is now bigger than Australia's entire GDP

$4.5 trillion in assets, against a GDP of roughly $3 trillion. Equivalent to about a fifth of the nation's total net worth — every home, mine, business and dollar combined.

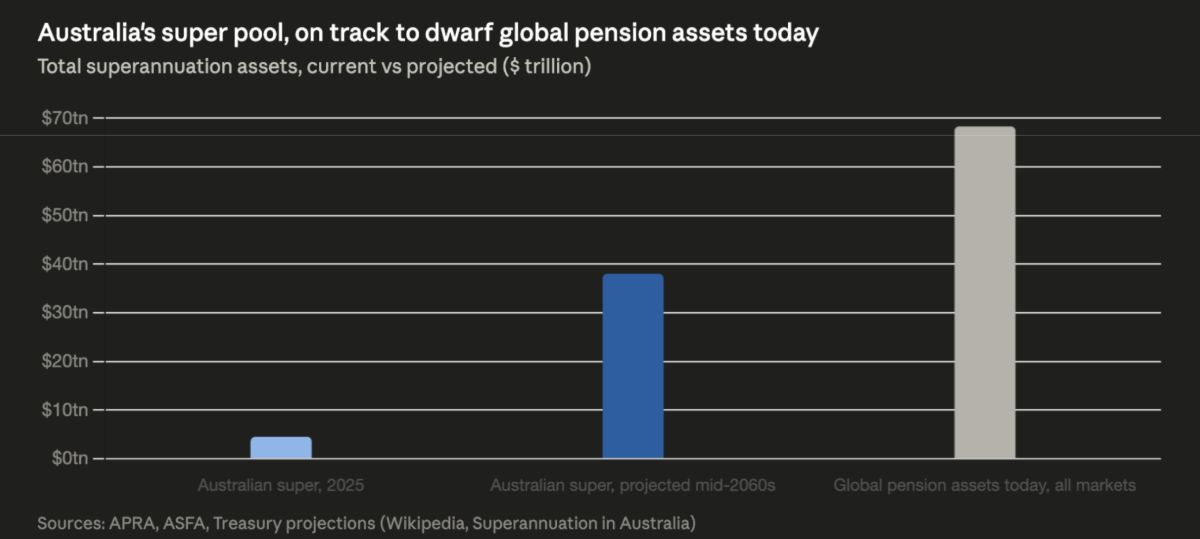

5. Australia is on track to hold more than half the world's pension assets

Treasury projects $38 trillion by the mid-2060s. Global pension assets today, across every major market on Earth, sit around $68 trillion. Which means one country of 27 million people is on track to hold more than half that combined total by itself.

6. Australia is about to out-save the UK and Canada — with a fraction of their populations

The country is set to overtake the UK's pension pool in 2030 and Canada's in 2031, becoming the world's second-largest behind only the US. Achieved by a country with a third the UK's population and two-thirds of Canada's.

7. Large super funds charged $10.2 billion in fees last year — about half of what Australian households spend on electricity

Fees paid within APRA-regulated funds in FY24: $4.4bn admin, $3.6bn investment. Total Australian household spending on electricity for the same period is around $20bn — so the cost of running compulsory super, on its own, comes to roughly half of what the entire country pays to keep the lights on.

8. Once SMSFs are counted, total super fees hit $34 billion — 1.6X Australia's foreign aid budget

That's the whole-of-system estimate for FY25. Most of the gap above the $10.2bn APRA figure comes down to scale economics: SMSFs carry largely fixed accounting and audit costs regardless of balance, so smaller self-managed funds pay proportionally far more to run than large pooled funds do.

9. 9 in 10 dollars paid to run super never touch the actual fund

Roughly 90% of the $9–10bn a year funds pay to service providers goes to external firms — custodians, consultants, asset managers — not the institution managing the accounts. Most of what gets called a ‘fund fee’ is really a payment to someone else.

10. Super fund directors are paid more than the median full-time salary — for a part-time job

Directors make $98,809 a year, on average, across 397 directorships. That's above the ~$90,000 median full-time Australian salary, for a role that is, for most directors, part-time.

11. $18.9 billion of Australians' super money is currently missing

It sits lost or unclaimed across 7.3 million accounts — an average of roughly $2,590 per account, waiting to be claimed.

12. 1 in 4 Australians is quietly paying double fees

23% of Australians hold two or more super accounts, often without realising it — each one charging its own admin and investment fees.

13. Employers didn't pay $6.25 billion in compulsory super they legally owed

That's the ATO's estimate for 2022–23 — about 6% of total Super Guarantee liability that year. Underpayment is typically caught through an audit or a worker complaint, sometimes years after the fact.

14. Super funds underperformed the sharemarket by roughly 6 percentage points

The All Ordinaries Accumulation Index — a simple, undiversified basket of Australian shares — returned 13.1% p.a. since 1990. Diversified, professionally managed, fee-charging balanced super funds returned 7.2–8% over almost the same window. Part of that gap reflects the defensive assets balanced funds hold to manage risk.

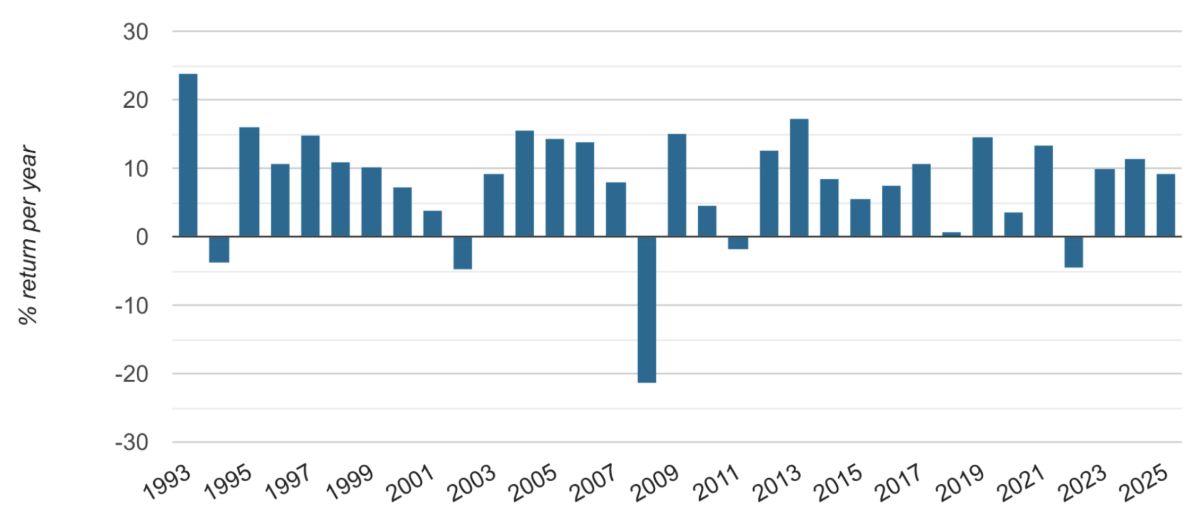

15. $1 invested in 1992 is worth $2.84 today

The value, in real terms, of $1 in the median balanced super fund since the system began — a 5.2% p.a. real return. Only five financial years have finished negative in 33: FY02, FY08, FY09, FY20 and FY22.

The next wave of unwitting investors?

I had no idea when I got my first fresh-off-the-boat paycheck that I had become an investor.

Many of those entering the workforce today likewise probably have little or no idea about the system, the assets, the returns and the fees — let alone the scale of it all.

Twelve percent of their pay will be invested in their super fund.

Perhaps in another 30 years it will be more.

Hopefully, they’ll quickly acquire the financial literacy and knowledge of the Australian system to understand where their money is going and what it’s doing.

This week's quote:

"The years teach much which the days never know."

— Ralph Waldo Emerson

Invest in knowledge,

Note: All figures and statistics presented here are accurate to the best of my knowledge, but I don't claim to be an authority on superannuation, and this newsletter is, of course, in no way financial, tax, or retirement advice. But you knew that.

Thom

The Benchmark

Read more: Are we on track for S&P 14,000?

Share: Forward this email to someone you know would appreciate it.

Become a reader:Subscribe to The Benchmark.

Enjoyed this issue?

Subscribe to The Benchmark

Weekly insights on markets, investing, and portfolio strategy.