The S&P 500 in 2034? (Pt. II)

In early 2024, I wrote about whether the easy money has already been made.

See, writer Richard Fisher argues that humans have evolved the capacity for long-term thinking, and yet almost never use it.

We default to the next news cycle, the next quarter, the next candle on the chart — what Fisher calls ‘dangerous short-termism’.

The case against short-termism, in April ‘24: a secular bull market, the kind that comes along maybe twice a century, with two veteran strategists — Robert Sluymer and Bank of America's Stephen Suttmeier — both pointing to the same 16-to-18-year cycle and arguing stocks could climb for another decade.

According to this view, Sluymer saw the S&P 500 reaching 14,000 by 2034 — about twice as high as it trades today.

But how does it get there?

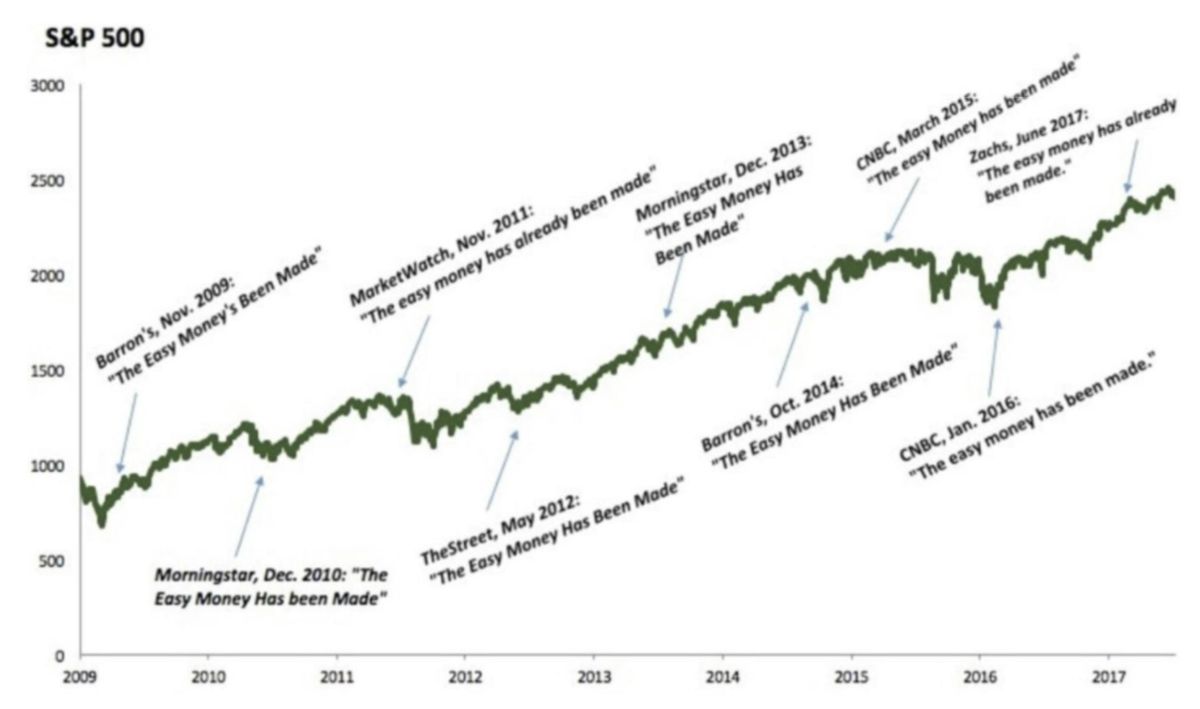

Well, you might have heard the phrase ‘markets climb a wall of worry’.

Between 2009 and 2017, financial media declared that ‘the easy money has already been made’ nine times.

And yet, all nine times, stocks continued their climb.

Well, today, in mid 2026, we’re revisiting this tension between short-term and long-term thinking about the stock market, and considering whether the easy money has perhaps now, finally, been made…

…or if stocks are currently just taking a minor pause before potentially pushing higher for another eight years.

Is the S&P 500 following the ‘secular bull market’ thesis?

In April 2024 when I wrote one of the first Benchmark emails, the S&P sat around 5,200.

It closed last week at 7,537.

That's a gain of roughly 45% in about two-and-a-half years.

Measured against Sluymer's 14,000 target, the index has now covered about a quarter of the distance — in roughly a quarter of the 10 years he gave it.

That's not a prediction the market will move in a straight line to 14,000 — no market ever has.

But it’s worth noting that the trajectory hasn't fallen apart in the two and a half years since these strategists made their case.

The song remains the same

As I write this, Bank of America is calling for the S&P to retreat to 7,100 by year-end.

They cite ‘speculation hitting extreme levels’ and warn of a valuation ‘snapback’.

Fundstrat's Tom Lee, who is broadly bullish with an 8,000-plus year-end target, went on CNBC to warn of a 10% to 20% drawdown between August and October — something that will ‘feel like a bear market’ before any rally resumes.

Strategists elsewhere are comparing this AI-driven rally to the late stages of the dot-com bubble.

This is the exact posture of the nine headlines from that old chart.

The so-called ‘easy money’ has been made. Hard times lie ahead.

Four new bear calls in 27 months

Since my 2024 piece, the same claim has been made at least four more times — each with a real, specific trigger.

August 2024, yen carry trade unwind: The Bank of Japan raised rates, a soft US jobs report spooked traders, and the unwinding of the yen carry trade tore through global markets.

The Nasdaq-100 fell 13% in weeks.

Fortune's actual headline: ‘How An Obscure Japanese Yen Trade Sparked A Global Market Meltdown — And Why The Worst Could Be Yet To Come’.

By the end of that week, the S&P had recovered every lost point.

January 2025, $589 billion DeepSeek panic: A Chinese startup called DeepSeek released an AI model reportedly trained for under $6 million.

Nvidia lost $589 billion of market value in a single session — the largest one-day loss in US stock market history.

The story was that the entire AI capex boom was about to unravel.

Nvidia is up roughly 76% since that day.

April 2025, Liberation Day recession calls: Trump's ‘Liberation Day’ tariffs triggered a 12% drop in the S&P over four trading days.

JPMorgan warned of recession.

Nine days later, the index rallied 9.52% in a single session — its best day since 2008.

It was positive for the year by mid-May, at new highs by late June, and is up more than 35% since the low.

February–March 2026, oil crisis & dotcom bubble fears: War broke out between the US, Israel and Iran. Oil spiked soared towards $110.

The Dow fell into correction, the Nasdaq dropped nearly 13%, and even gold — the asset that's supposed to zig when everything else zags — fell 16% in days.

‘US tech pullback mirrors late stages of dotcom era’, ran one headline. By April, the market had recovered most of the March losses.

These are just four recent ‘easy money has already been made’ calls.

And just like the nine in the chart I shared above, stocks brushed each aside and promptly resumed their charge higher.

The case for bearishness in 2026

None of the above necessarily proves the bears wrong.

A few months back, I compared the current AI IPO pipeline to the dot-com bubble and bust — the difference this time being that real revenue, not just narrative, appears to be driving the AI companies’ growth.

CoreWeave, the company I flagged as the bellwether to watch, has swung more than 50% in either direction since its listing — hardly the price action of a confident market with a steady bid.

Fear, uncertainty and doubt abound.

And there are genuine risks stacking up right now: valuations are stretched to levels last seen in 1999–2000.

Pieter Levels’ newly-launched Bubble Detector tool makes it clear:

Five overvalueds and two cautions. Worth noting, for sure.

The ten largest S&P 500 companies now account for close to 40% of the index's total value, which magnifies the damage from any single stumble.

Much of the current AI buildout is increasingly debt-financed, echoing the telecom overbuild that preceded the dot-com bust.

And a new, less predictable Federal Reserve chair has traders pricing in rate hikes rather than cuts for the first time in years.

None of that guarantees anything. But all of it is worth taking seriously.

Say the easy money has been made enough times, and at some point, you will be proven correct.

It's also worth noting what's different about this cycle compared to the nine calls between 2009 and 2017.

Those years were mostly about recovering from a financial crisis — the worry was generally always some version of ‘this recovery is fake’.

The four alarms since 2024, on the other hand, have each had a distinct, external trigger: a central bank decision, a foreign AI lab, a trade policy, an actual regional war. That's arguably a higher bar for the bull case to keep clearing, not a lower one.

The good thing about bad calls

None of the ‘easy money’ alarms above were foolish calls.

JPMorgan wasn't reckless to flag recession risk in April 2025. DeepSeek posed a genuinely important question about AI spending. Being uncomfortable and being wrong turned out, each time, to be two different things — and markets have a gift for making them feel identical while you're living through it.

I quoted Warren Buffett in my April ‘24 piece: the market moves money from the impatient to the patient.

The trickier version of that idea is that patience doesn't feel like a strategy while you're using it.

It feels like doing nothing while everyone around you is reacting to something — checking prices, reading the same headline and reactions in five different feeds, wondering if this is the one that's real.

But doing nothing, as you’ll see here, can be key to immense investment returns.

Fisher's point about short-termism isn’t really about markets.

It’s about a species that's very good at reacting to this week, but very bad at thinking in years and decades.

This week's quote:

"We suffer more often in imagination than in reality."

— Seneca, Letters to Lucillus

Invest in knowledge,

Thom

The Benchmark

Read more: 165 millionaires are casting their votes.

Share: Forward this email to someone you know would appreciate it.

Become a reader:Subscribe to The Benchmark.

Enjoyed this issue?

Subscribe to The Benchmark

Weekly insights on markets, investing, and portfolio strategy.