What if inflation is a feature, not a bug?

I’ve written recently about fiat currencies’ appalling failure rate throughout history, and how successive cuts between paper money and gold have marked precipitous falls in purchasing power for everyday people.

Today, we’re going to explore the other side of the devaluing coin. The steadily devaluing coin, that is — as opposed to the hyperinflation victims that collapse economies.

Because when we criticize fiat currency, it’s usually an inflation criticism.

As in, how can it possibly be a good thing that the cash in my bank account this year will be worth 33% less 10 years from now?

It’s easy to look at that fact and jump directly to arguing fiat is evil, unfit for purpose, a mechanism of state oppression, a symptom of fiscal excess and so on.

But making this argument involves making a huge assumption:

That fiat currency’s purpose is to be a store of value.

As you’re about to see, fiat’s purpose is entirely different — especially today.

So let’s look for the good in the fact that the cash in our accounts loses economic power by the day.

Money: What is it good for?

There are three main use cases for money.

1. Medium of exchange: Money can be a go-between. It allows individuals, businesses, institutions and governments to trade.

2. Unit of account: Money can be a yardstick. It’s a common language of economic calculation, which allows us to compare the value of different things.

3. Store of value: Money can be a time machine. It lets you store value you create, for future use.

Different forms of money suit different use cases to a greater or lesser extent.

Gold is an excellent store of value, for example. It’s rare and therefore difficult to inflate by increasing supply. It never rusts or decays.

You could argue it’s a decent unit of account, too, given all the fiat currencies that used a gold standard.

But you could not argue gold is a good medium of exchange. Because not only is there relatively little of it, but it’s heavy and bulky, which makes settling transactions in physical gold exceedingly difficult.

Whereas cash, on the other hand, is a great unit of account and medium of exchange — especially in the digital form we’re used to these days.

Compared to gold, you can settle transactions fast and with almost no physical work.

It’s this distinction which brings us to the Triffen Dilemma.

The paradox of competing economic interests

We often talk about a nation taking its currency off the gold standard as a fatal fiat flaw.

Because history shows that up to 99.9% of currencies fail to survive once the link between the paper and the precious metal severs.

This perspective leans heavily on assessing fiat currency in terms of its suitability as a store of value.

But when you’re supplying the world’s reserve currency, as the US does, store of value is not first, or even second, priority.

The priority is to be the globally-accepted medium of exchange and unit of account.

On the one hand, this is the store of value trend for the dollar:

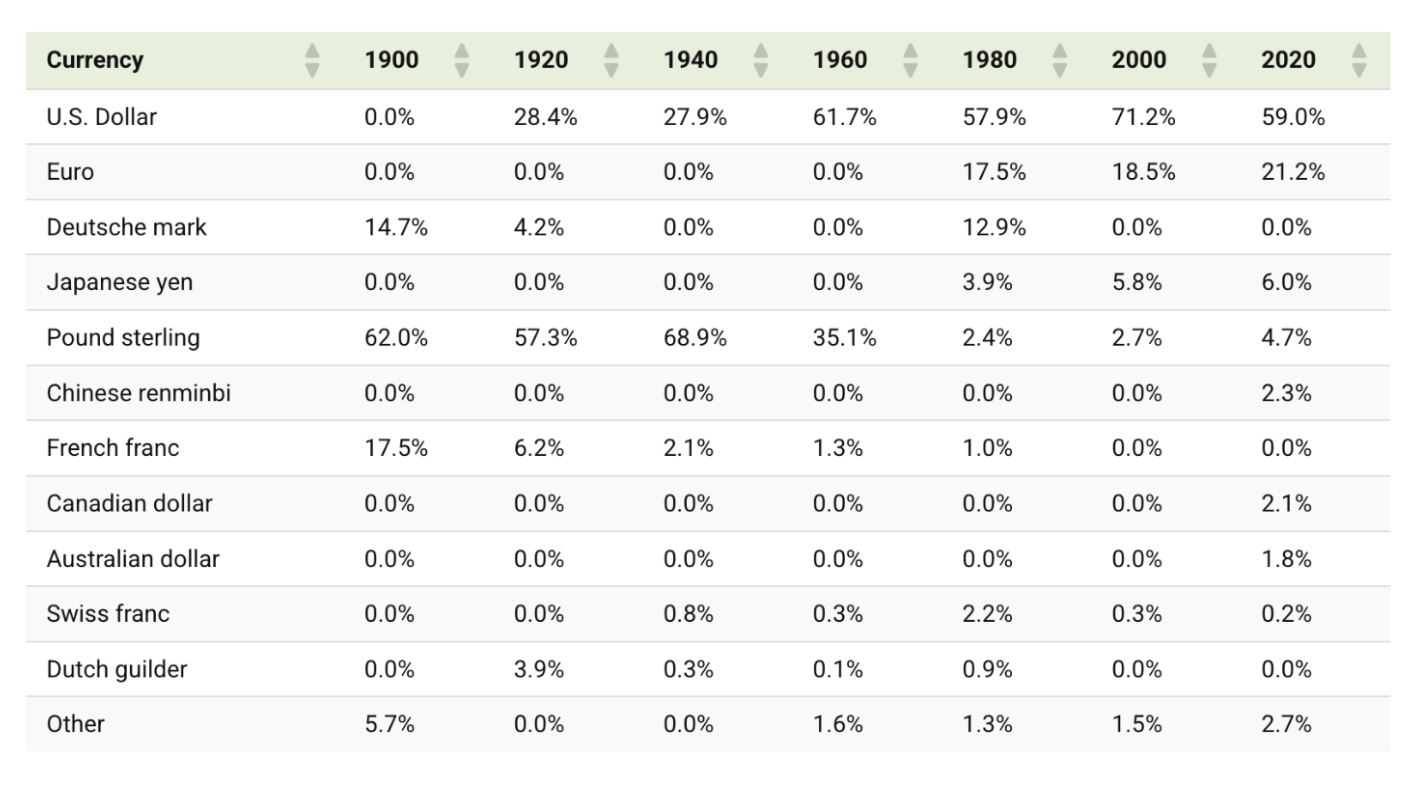

On the other, here’s the dollar’s global dominance over 120 years — expressed as a percentage of currency reserves held across the world.

From 0.0% in 1900 to 59% in 2020.

In 2026, USD dominance is steady at about 57%.

By definition, a reserve currency has to be everywhere.

Which means you need a lot of it.

Which means maintaining a currency as a store of value isn’t as important as increasing its supply and usage.

This is the paradox which Belgian-American economist Robert Triffin described in the 1960s, as the world shifted to a US Dollar standard.

Triffen noted that a country whose currency is the global reserve had to supply the world with its currency in order to fulfill foreign exchange and reserve demand.

To do this, the reserve currency nation must run a trade deficit — it must buy more than it sells, so that more of its currency flows out than in.

The Triffen Dilemma expresses the fact that you must expand money supply and diminish purchasing power to maintain or strengthen reserve currency status.

The dollar bug is the feature

The US Dollar has lost a third of its purchasing power over the past decade.

But, it remains the reserve currency for most of the world (read about the previous title holders and potential challengers).

Securing reserve status was President Nixon’s objective when he took the dollar off the gold standard in 1971.

By removing the condition that every dollar be backed by physical gold reserves — remember, difficult to produce and difficult to exchange — Nixon gave the US carte blanche to flood the global economy with dollars.

In this context, inflation isn’t some nefarious means of confiscating wealth from citizens.

It’s a pressure-release valve, allowing liquidity-on-demand dollars to keep America’s trading partners using her currency.

Consider, for example, if the US had remained on the gold standard, and not printed a single dollar beyond its physical gold reserves.

The dollar might not have lost so much of its value. But nor would it have the economic dominance and reach it does today.

And there’s more to the pro-inflation narrative than just reserve currency status.

According to Austrian economist Ludwig von Mises, a steadily-devaluing fiat currency serves another, higher, purpose.

Inflation as innovation incentive

Von Mises was a leading economist from the Austrian School of Economics, a group who emphasized the importance of a price system and free markets.

He viewed the stock market as the heart of the capitalist system, and the centre of innovation.

Its the place where entrepreneurs raise capital to fuel progress.

The place where investors deploy capital to generate a better return than by holding cash.

In this way, a free floating fiat currency which steadily loses purchasing power acts as an incentive.

It drives innovation and attracts investment.

Because holding cash is pretty much a guaranteed way to lose wealth, whereas investing it makes growing wealth possible.

Medium of exchange > store of value

Fiat currency is not designed to be a store of value.

It’s designed to facilitate trade and stimulate economic growth.

Other assets have other purposes.

Consider Bitcoin.

Because there’s a finite supply of 21 million coins, there can be no inflating the supply beyond that hard cap.

This makes Bitcoin ‘cool’ money.

Similar to gold, there is no structural pressure to move it.

This could, in theory, lead to a liquidity trap; money might only ever enter the network, and never leave.

The absolute scarcity might mean it would never make sense to sell an asset whose price only ever increases over time.

Fiat, by comparison, is ‘hot money’.

The slow bleed of purchasing power (inflation) provides the pressure and incentive to spend and invest.

So yes, the US Dollar has lost 99% of its purchasing power.

There’s no arguing that it’s not a terrible store of value — even if it is one of the few fiat success stories.

But the argument for a slow-bleeding dollar is nothing to do with storing value.

Leave that to gold and bitcoin.They are scarce, inflexible assets designed to act as time machines for storing energy as capital.

Steadily-inflating fiat is, from this perspective, fuel for trade, innovation and growth — and, in the case of the US Dollar, reserve currency status.

This week's quote:

“Only money that goes out of date like a newspaper, rots like potatoes, or melts like iron when exposed to the heat of the furnace, can be a suitable medium of exchange... for such money will not be hoarded.”

— Johann Silvio Gesell

Invest in knowledge,

Thom

The Benchmark

Read more: Edison and Ford invented Bitcoin in 1921?

Share The Benchmark: If you've enjoyed reading, forward this email to someone you know would appreciate it.

New here? Subscribe to The Benchmark.

Enjoyed this issue?

Subscribe to The Benchmark

Weekly insights on markets, investing, and portfolio strategy.