Tax to the future

This Benchmark is about the proposed Australian capital gains tax law changes. It just won’t feel that way at first.

In 1987, Ireland was broke.

Unemployment was above 17%. The country was haemorrhaging people — 70,000 left in that year alone.

The national debt was approaching 120% of GDP. A generation of young Irish people assumed they would spend their working lives somewhere else.

Then the government made a bold tax decision.

Ireland set its corporate rate at 12.5% — the lowest in Europe — and cut capital gains tax from 40% to 20%. The message was simple and explicit: If you want to deploy capital, Ireland will treat it better than anywhere else on the continent.

Capital responded the way capital tends to respond to that kind of invitation.

Foreign direct investment flows rose from 2.2% of GDP in 1990 to 49.2% by 2000.

Intel, Microsoft, Apple, Google, and Facebook built their European headquarters in Dublin. GDP growth ran between 7.8% and 11.5% a year for five straight years.

In other words, the so-called Celtic Tiger wasn't an economic miracle. It was the outcome of an incentive structure.

The lesson is simple. Capital goes where it's treated best.

Australia has just proposed to make it considerably more expensive to deploy capital.

28 Years Later

On 12 May 2026, Australian Treasurer Jim Chalmers announced the most significant tax reform package in more than a quarter century.

The 50% Capital Gains Tax discount — introduced by John Howard in 1999 — will be replaced with an inflation-indexed discount from July 1, 2027. A minimum 30% tax on capital gains will apply. Negative gearing — where you deduct investment property losses against your personal income — will be limited to new residential builds.

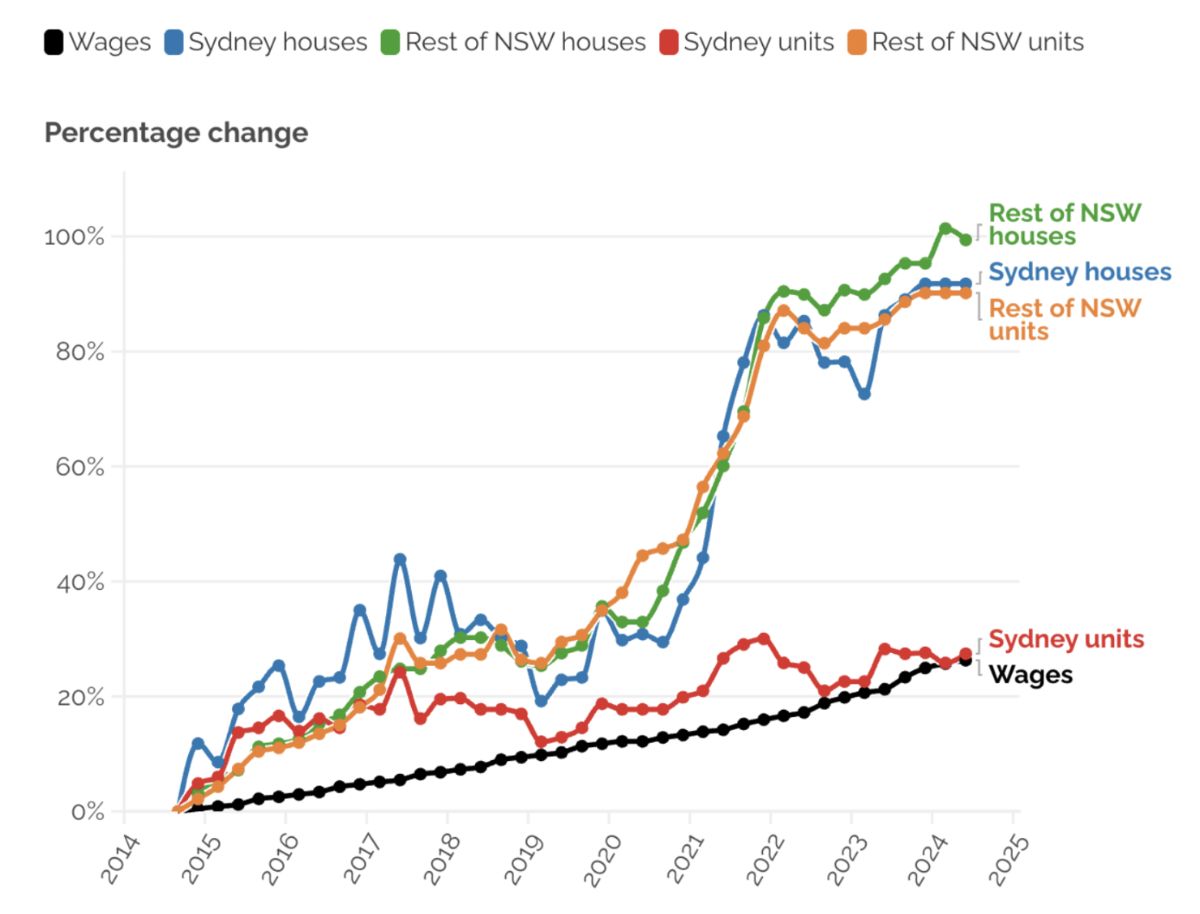

The government’s stated aim is housing affordability. The 1999 discount turbocharged speculative property investment, house prices and wages uncoupled entirely, and the home ownership rate among 25-34 year olds fell 7 percentage points over twenty years.

This chart from SBS shows you the divergence playing out New South Wales:

On those terms the reform is defensible; the 1999 change was a mistake. Before Howard's discount, house prices rose roughly in line with incomes. After that, they didn't. Hence the change.

But for high-income investors on the 47% marginal rate, the effective CGT rate roughly doubles under the government’s proposed new system.

The reaction has been as you’d expect — check out this collection of Australian front pages from The Guardian:

That makes Australia's top CGT rate one of the highest in the developed world.

And it won’t just apply to property. It will apply to everything.

But if it’s all about improving housing affordability, the changes are necessary — this is the government’s argument.

Capital gains tax is, in their view, the single lever with which they can bring runaway property prices back within reach of those citizens who can’t afford to enter the market.

Let’s explore that idea on the other side of the Tasman Sea.

The land of the tax-free capital gain

New Zealand, my home country, has never had a broad capital gains tax. Not even after its own Tax Working Group — chaired by former Finance Minister Sir Michael Cullen — formally recommended one in 2019.

Then-Prime Minister, Jacinda Ardern, killed it. “While I have believed in a CGT,” she said, “it's clear many New Zealanders do not”.

Who would have thought?

New Zealand kept its benign tax environment for property investors. No CGT.

Unrestricted negative gearing. The full treatment.

The International Monetary Fund subsequently ranked New Zealand at the top for housing unaffordability in the OECD. Its house price-to-income ratio hit 142 in late 2021 — among the highest ever recorded in the developed world. My country also has one of the highest homelessness rates in the OECD.

So Australia had a generous CGT regime and still had a housing crisis.

New Zealand had no CGT and still had a housing crisis.

Cullen's own review actually conceded — a CGT would have only a limited, and possibly even inflationary, impact on house prices.

The primary drivers were supply constraints: zoning, infrastructure, planning systems built for a smaller country.

So you can argue that CGT is not the primary lever. In either direction.

It’s also important to contextualize the Australian CGT proposal within a broader trend of nations attempting to tax themselves wealthy.

When trying to raise $146 million loses you $594 million

The clearest modern data point on what happens when you raise the cost of holding capital comes not from Australia or New Zealand, but from Norway.

In 2022, Norway's government raised its wealth tax by a modest 0.25 percentage points — from 0.85% to 1.1%. It projected the change would raise an additional $146 million annually.

Instead, individuals worth $54 billion left the country. The result was a $594 million annual loss in tax revenue — four times the projected gain.

More than 100 of Norway's top 400 taxpayers, representing half that group's total wealth, now live abroad, mainly in Switzerland. I wrote about the mechanics of the country taxing itself poorer here.

To be clear: Norway's wealth tax and Australia's CGT reform are different instruments. A wealth tax is an annual levy on the stock of assets; CGT is triggered only on realization. The lock-in effect of higher CGT — investors holding assets longer to defer the tax event — is different from the capital flight dynamic of an annual wealth tax.

But the underlying principle holds. When the expected after-tax return on capital in a jurisdiction falls materially, capital reprices its options, even if it doesn’t leave overnight.

Canada learned this lesson. The country proposed a CGT inclusion rate rise in 2024. The backlash was swift enough that it was cancelled in 2025 — and Canada's international tax competitiveness ranking rose upon cancellation.

The property narrative as a Trojan Horse?

While the Australian government claims it has designed this reform with young Australians and prospective property owners in mind, the reality is that it impacts everybody.

Within days of the budget, Australian startup founders launched an open letter to the Prime Minister. The signatories — including co-founders of Linktree, me&u, and others — made a specific and pointed argument: The CGT discount isn't just a property subsidy. It's the economic logic that makes startup equity worth sacrificing for.

‘People bet their careers that in return for their sacrifice today, they will be rewarded through stock options when that startup becomes the next big tech success story,’ one founder wrote.

‘By axing the 50% CGT discount, Treasurer Jim Chalmers has launched a direct attack on that incentive to innovate.’

The government acknowledged the problem. Chalmers flagged potential carve-outs for high-growth companies, describing the startup sector as ‘the hope of the side when it comes to dynamism and productivity’.

Startup founders haven’t been the only group to react strongly to the government’s proposals.

Only time will tell if and how the changes might morph before passing into law.

Where does the capital go now?

This is the question that matters for investors — and it doesn't have a clean answer yet.

Some capital will likely now flow into superannuation, where the tax treatment remains concessional.

Some into new residential builds, which retain both the CGT discount and negative gearing under the new rules — a deliberate supply-side nudge.

Some possibly offshore, gradually, as Australian founders and investors weigh up Singapore, Dubai, and other jurisdictions where capital is treated better.

Perhaps the proposed reforms will restore something that was genuinely broken in 1999.

Perhaps Howard's discount was a policy mistake with a 28-year hangover.

Perhaps Jim Chalmers is right to unwind it.

But Ireland's, New Zealand's, and Norway's stories are worth keeping in mind.

Ireland’s transformation began with a government that understood one thing clearly:

Capital has options. Treat it well, and it builds things. Tax it punitively, and it finds somewhere else to go.

New Zealand's crisis is a reminder that the property problem is more complex than just tax.

Norway's lesson is the sharpest of all: A modest increase in the cost of holding capital, applied to a small number of people, produced a revenue loss four times larger than the projected gain. The government reached for more. It got less.

Australia is not Norway, of course. The proposed CGT change is not a wealth tax.

The capital flight risk is real, but not acute. At least not yet.

What is acute is the signal. A top CGT rate approaching 47%, applied to shares, startups, and business assets alike, tells capital something about the cost of building, investing, and taking on risk in Australia.

The government is attempting something genuinely difficult — rebalancing a tax system without triggering the very capital flight it's trying to redirect.

Whether it threads that needle might depend less on the policy itself, and more on what investors decide to do next.

This week's quote:

"For every complex problem there is an answer that is clear, simple, and wrong."

— H.L. Mencken

Invest in knowledge,

Thom

The Benchmark

Read more: The $3.12 trillion (or more) flood primed to hit the stock market.

Share: Forward this email to someone you know would appreciate it.

New here? Subscribe to The Benchmark.

Enjoyed this issue?

Subscribe to The Benchmark

Weekly insights on markets, investing, and portfolio strategy.