For Australian investors, 30 June matters.

Once the financial year ends, your investment activity for that year is locked in. You can still prepare reports, check your records and work with your accountant, but some decisions that could affect the final tax outcome may no longer be available.

That is why tax time can catch investors out.

Not because they are trying to do the wrong thing.

But because they leave the record-checking, parcel selection, ETF statements and capital gains review until too late.

In this article, we’ll cover five common tax traps Australian investors should check before the end of financial year, based on our latest Navexa video.

Please note: This article is general information only. It does not recommend any tax strategy, sale decision or investment action. Always speak with a qualified accountant or tax professional about your personal circumstances.

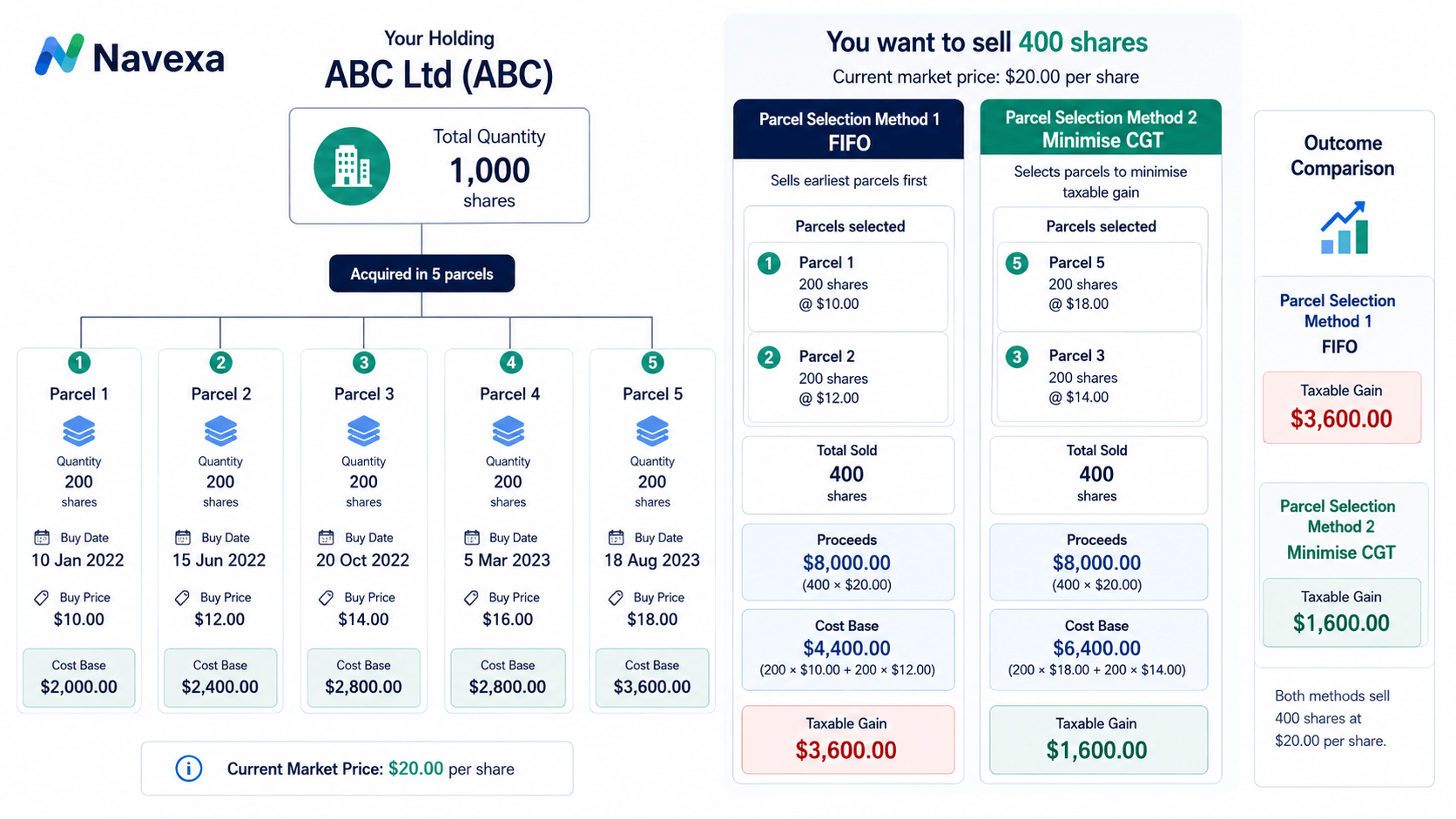

1. Defaulting To FIFO Without Checking The Impact

FIFO stands for first in, first out.

In simple terms, if you bought the same share or ETF multiple times, FIFO assumes the first units you bought are the first units you sold.

There is nothing automatically wrong with FIFO.

The problem is using it without checking whether it reflects the outcome you want for that financial year.

For example, say you bought the same holding across multiple parcels over several years. Some parcels may have a low cost base. Some may have a higher cost base. Some may qualify for the CGT discount. Some may not.

When you sell part of that holding, the parcel selection method can affect the realised capital gain or loss.

In Navexa, investors can compare different CGT allocation strategies, including:

- FIFO, or first in, first out

- LIFO, or last in, first out

- Minimise gain

- Maximise gain

- Minimise CGT

- Per-holding strategy overrides

Different strategies can produce very different outcomes for the same sale.

But this is not about saying one method is always better than another.

It is about visibility.

A strategy that makes sense in one financial year may not make sense in another. For example, an investor may want to review a different outcome in a low-income year compared with a high-income year. Or they may want to understand what happens if they realise a gain now versus later.

The key point is simple:

Do not assume FIFO is the only option without checking the impact.

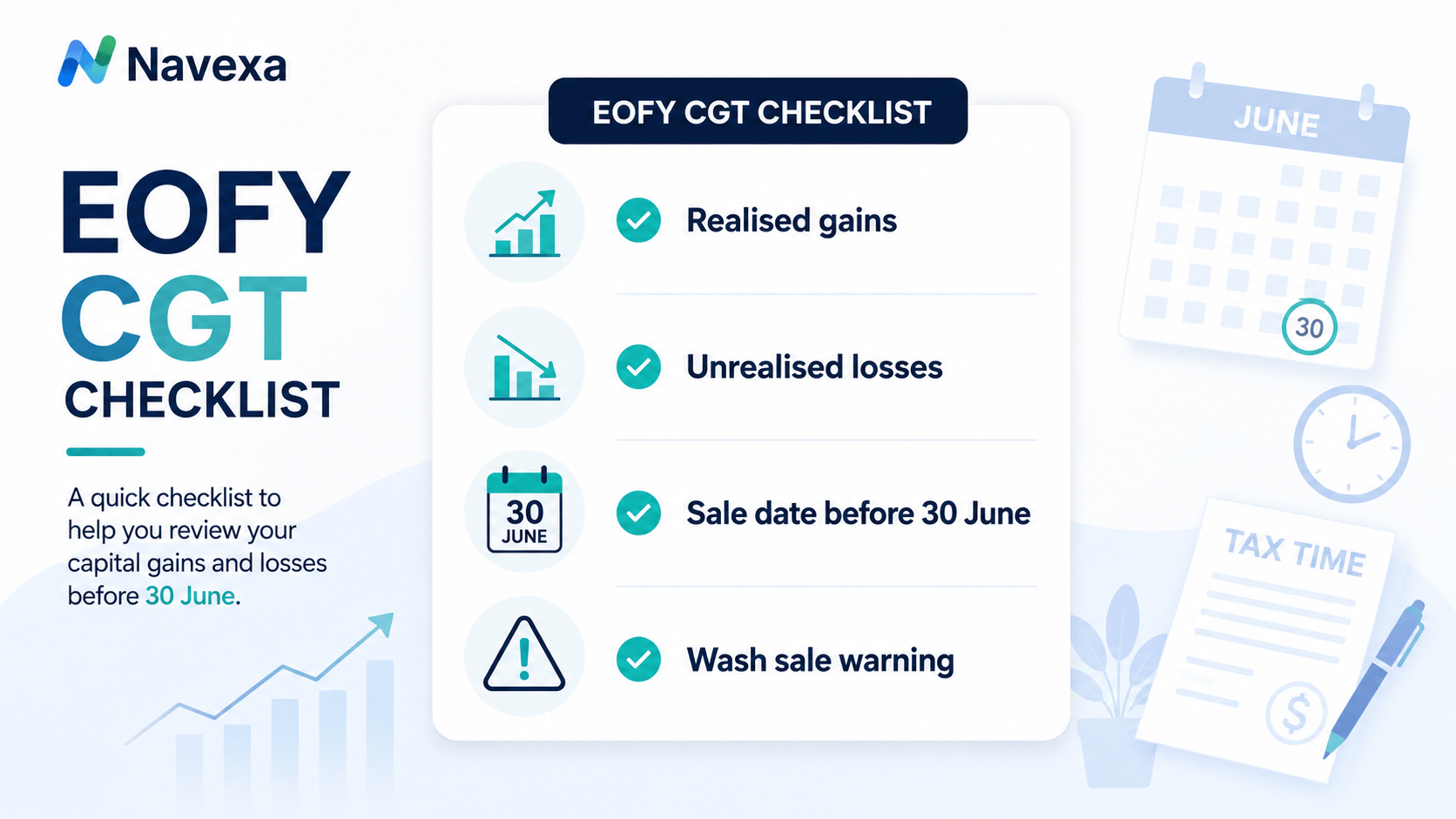

2. Not Reviewing Capital Losses Before EOFY

Capital losses can generally be used to offset capital gains.

But the important word is realised.

If an investment is down on paper, that does not automatically create a capital loss for tax purposes. In most cases, the loss is only realised when the investment is sold.

That is why investors often review unrealised gains and losses before 30 June.

If you have realised gains during the year, you may want to understand whether there are any unrealised losses in your portfolio. That does not mean you should automatically sell something just because it is down. Selling an investment should still make sense for your circumstances and broader plan.

It does mean you should know where you stand before the financial year closes.

Inside Navexa, the Unrealised Gains report can help investors see what may happen if holdings were sold at current market prices. This can help investors and their advisers review potential gains and losses before decisions are made.

There is also an important warning here.

Selling an asset at a loss and then quickly buying the same or a similar asset back may raise wash sale concerns. The ATO has warned about wash sales, where a taxpayer creates a capital loss while maintaining a substantially similar investment position. Public reporting has also noted that the ATO can use data analytics to identify this behaviour.

So this is not about gaming the system.

It is about understanding your actual tax position before 30 June and speaking with a professional before making tax-related decisions.

3. Poor Recordkeeping

Good recordkeeping is boring.

It is also one of the most important parts of investing.

If the ATO or your accountant asks how you calculated your capital gains, losses, cost base, dividend income or ETF adjustments, you need records that support the numbers.

This becomes harder as your portfolio grows.

A simple portfolio might only have a few buy and sell trades.

A real portfolio may include:

- Regular buys

- Partial sells

- Dividend reinvestment plans

- ETF distributions

- AMMA or AMIT statements

- Broker transfers

- International holdings

- Currency movements

- Crypto assets

- Corporate actions

- Multiple brokers over time

Broker transfers are a common problem.

When you move holdings from one broker to another, the new broker may receive the current holding quantity. But it may not receive the full trade history behind that holding.

That matters.

If you bought 100 shares across ten different parcels, including dividend reinvestments, your future CGT calculation may depend on those original parcels.

If that history is missing, your records may not tell the full story.

This is one reason Navexa is designed to keep a central record of your portfolio history across holdings, brokers and asset types.

It helps investors track the details that can be difficult to maintain manually over time.

4. Assuming Your Broker Has Everything Covered

Brokers are built to help you buy and sell investments.

They are not always complete portfolio tracking, performance reporting or tax reporting systems.

Your broker may show your current holdings, market value and recent trades. But that does not always mean it gives you the full portfolio picture.

For example, your broker may not clearly show:

- Long-term annualised performance

- Total return including dividends and distributions

- Dividend reinvestment history

- Portfolio-wide realised and unrealised gains

- Currency impact on international holdings

- Complete tax reporting across multiple brokers

- Cost base history for transferred positions

- AMIT cost base adjustments for ETFs

This can lead to misleading conclusions.

A holding might look flat on price alone, but the total return may look different once dividends and distributions are included.

A US share might be up in USD terms, but your AUD return may look different once currency movement is included.

A transferred holding might look correct by quantity, but still be missing original purchase history.

That is why relying only on your broker can leave gaps.

Navexa helps investors look beyond one broker account by tracking performance, income, trades, cost bases, realised gains, unrealised gains and currency impact in one place.

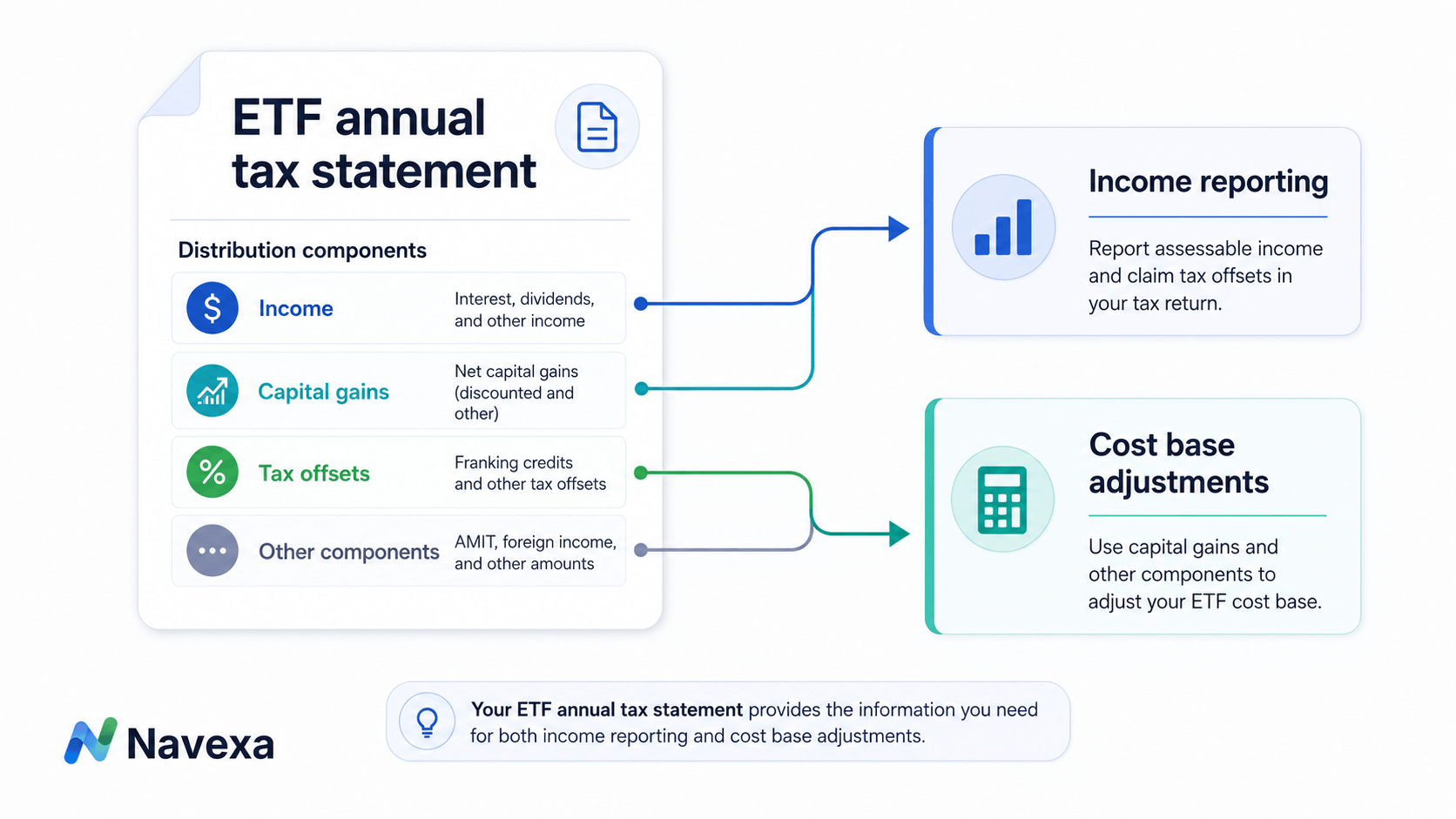

5. Not Tracking AMIT Cost Base Adjustments

This one is especially important for ETF investors.

Each year, many ETF investors receive an annual tax statement. Depending on the fund structure, this may include AMMA or AMIT information.

These statements can include several tax components, such as:

- Franked distributions

- Unfranked distributions

- Foreign income

- Capital gains

- Tax offsets

- Cost base increases

- Cost base decreases

The cost base adjustment lines matter.

They can affect the cost base of the ETF units you own. That cost base can then affect the capital gain or loss when you eventually sell.

This becomes messy when you have been dollar-cost averaging into an ETF over time.

For example, if you bought ETF units every month for three years, you may have 36 separate parcels. An annual cost base adjustment may need to be applied across the relevant parcels.

Then next year, there may be another statement.

And the year after that, another one.

If these adjustments are not tracked properly each year, the problem can build up.

That is why ETF annual tax statements are not just paperwork. They can affect income reporting, CGT records and future cost base calculations.

Navexa helps Australian investors record ETF tax statement information, including AMIT and AMMA details, so the relevant components can be reflected in portfolio records.

Why This Matters Before 30 June

The big takeaway is this:

Tax-time problems are easier to review before 30 June than after it.

Once the financial year closes, you can still report correctly. But some choices that may affect the outcome may no longer be available.

Before EOFY, Australian investors may want to check:

- Which CGT allocation strategy is being used

- Whether FIFO is being applied by default

- Whether there are realised gains for the year

- Whether unrealised losses need to be reviewed

- Whether any sale decisions could raise wash sale concerns

- Whether dividends and distributions have been recorded

- Whether broker transfers left missing trade history

- Whether ETF AMIT or AMMA statements have been entered

- Whether reports are ready to share with an accountant

None of this means making rushed investment decisions.

It means having better information before the year closes.

How Navexa Helps Australian Investors At Tax Time

Navexa is built to help investors keep cleaner portfolio records throughout the year.

Instead of piecing together broker exports, spreadsheets, annual statements and old emails at tax time, Navexa helps track key portfolio information in one place.

That includes:

- Trades

- Holdings

- Dividends

- Distributions

- Dividend reinvestments

- Cost bases

- Realised gains

- Unrealised gains

- Currency impact

- Portfolio performance

- CGT reporting

- ATO myTax reporting

- AMIT and AMMA statement information

Navexa also lets investors compare CGT strategies, such as FIFO, LIFO, Minimise Gain, Maximise Gain and Minimise CGT.

That can help investors and their advisers better understand potential outcomes before making decisions.

Navexa does not provide personal tax advice. The platform helps organise and report portfolio information so you can review it and share it with a qualified professional.

Watch The Full Video

You can watch the full Navexa video here:

https://www.youtube.com/watch?v=5JsZo3usy_A

For more portfolio tracking, tax-time and investing walkthroughs, you can follow Navexa on YouTube here:

https://www.youtube.com/@navexa-tracker

Frequently Asked Questions

What are common tax traps for Australian investors before EOFY?

Common traps include defaulting to FIFO without checking the impact, not reviewing capital losses before 30 June, poor recordkeeping, assuming your broker has all the information, and not tracking ETF AMIT cost base adjustments.

Is FIFO always the right CGT method?

No. FIFO is one method, but it is not automatically the right method for every investor or every financial year. The right approach depends on your records, the parcels sold and your personal circumstances. Speak with an accountant or tax adviser before making tax decisions.

Can capital losses offset capital gains?

Capital losses can generally be used to offset capital gains, but the loss usually needs to be realised. If a holding is only down on paper and has not been sold, it may not create a capital loss for that financial year.

What is a wash sale?

A wash sale generally involves selling an asset to create a tax loss, then reacquiring the same or a similar asset while keeping a substantially similar investment position. The ATO may treat this as tax avoidance, so investors should seek professional advice before selling and repurchasing assets for tax reasons.

Why might my broker records be incomplete?

A broker may show your current holdings and recent trades, but it may not have full history from previous brokers, dividend reinvestments, registry activity, cost base adjustments or older transactions. This can matter when calculating gains, losses and performance.

Why do AMIT cost base adjustments matter?

AMIT cost base adjustments can change the cost base of ETF units. That cost base may affect the capital gain or loss when you eventually sell. If adjustments are missed year after year, the recordkeeping problem can build over time.

Can Navexa help with tax reporting?

Navexa helps Australian investors track portfolio records, income, realised gains, unrealised gains, CGT strategies, ATO myTax reporting and AMIT or AMMA statement details. You should still review your reports and speak with a qualified tax professional about your own situation.

Disclaimer

This article is general information only and does not constitute financial, legal or tax advice. Navexa does not recommend any specific investment, sale decision, tax strategy or course of action. Tax outcomes depend on your personal circumstances, portfolio records and applicable tax rules. Always speak with a qualified accountant or tax professional before making tax-related decisions.