We recently ran an EOFY ETF tax webinar with Pearler, and the chat made one thing very clear.

Many investors know they need to report ETF income.

But many are still unsure about the bits sitting underneath it.

The ETF tax questions investors kept asking

These came up during the webinar and are where ETF tax records can get confusing.

What is an AMMA statement?

Is that the same as an AMIT statement?

Why doesn't the cash distribution match the taxable income?

What is an AMIT cost-base adjustment?

Do you still need to record it if you haven't sold?

When you eventually sell, how do you know which parcels were sold?

These are good questions. They’re also exactly where ETF tax can get messy if your records are not kept up to date.

So this article is a plain-English recap of the main points from the webinar.

You can watch the full session below, download the slides, or use this as a simple guide to the records ETF investors may need to keep.

The simple version

ETF tax is not just about the cash that lands in your bank account.

That cash payment is only one part of the story.

For tax reporting, an ETF distribution can include income, franking credits, foreign income, foreign tax credits, capital gains from within the fund, and cost-base adjustments.

Some of those amounts may appear in your ATO pre-fill.

Some may not.

And the parts that are not obvious at tax time can still matter later, especially when you sell.

The key point is simple:

Your ETF tax records are not just about what you received this year. They also help support future capital gains calculations.

The cash payment is not always the full tax story

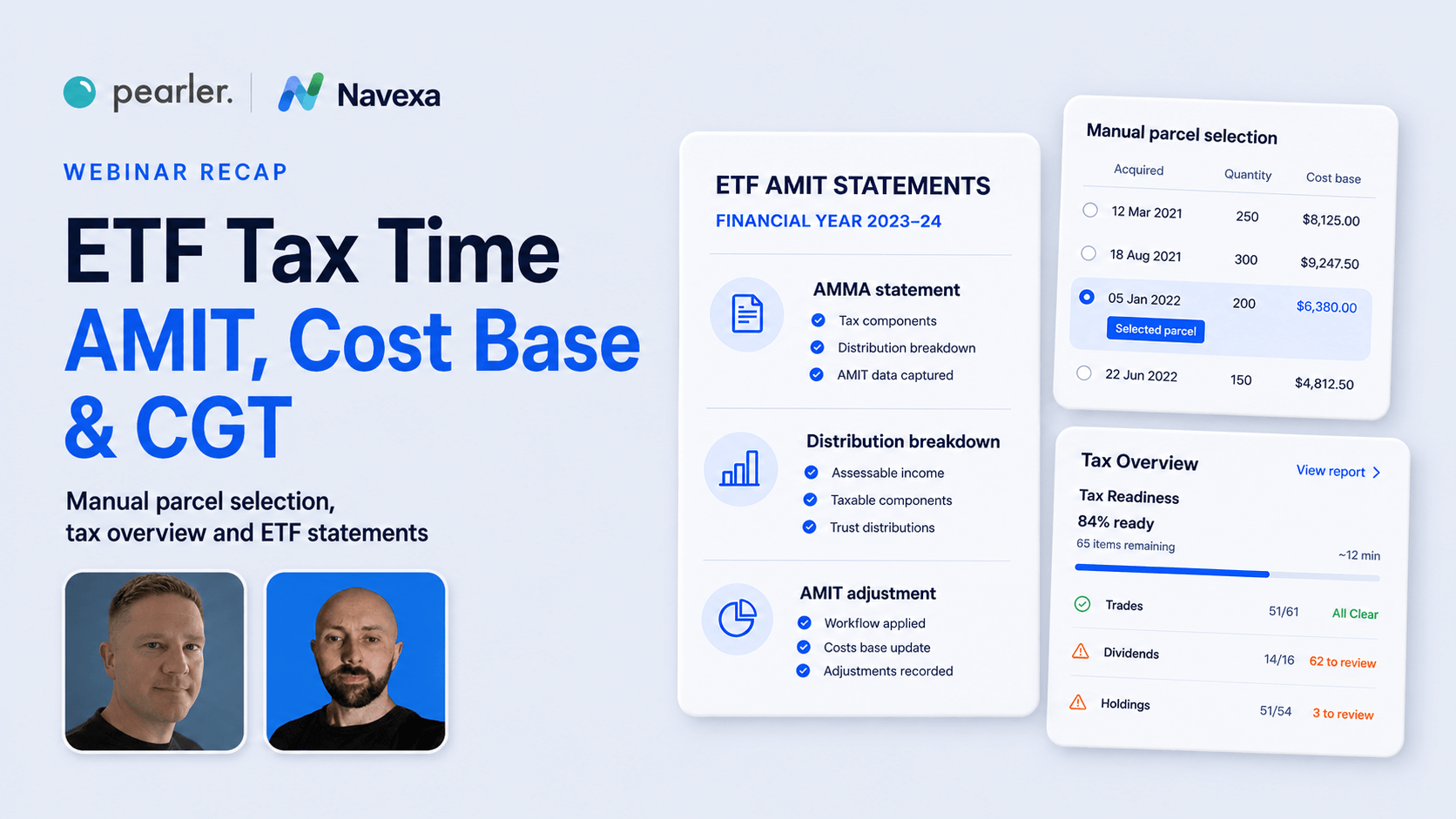

An ETF distribution may land in your bank account as one payment, but your AMMA statement can split it into several tax components.

What is an AMIT or AMMA statement?

AMIT stands for Attribution Managed Investment Trust.

AMMA stands for AMIT Member Annual Statement.

In plain English:

- AMIT is the tax framework under which many managed funds and ETFs operate.

- The AMMA statement is the annual tax statement you receive as an investor.

You will usually receive an AMMA statement for each relevant ETF you hold. For many Australian ETF investors, these statements become available after the end of the financial year, often around August or September.

The AMMA statement tells you what the fund has attributed to you for tax purposes.

That matters because an ETF can earn different types of income inside the fund during the year. The fund then attributes your share of those tax components to you.

This can include things like:

- Australian income

- Franking credits

- Foreign income

- Foreign income tax offsets

- Capital gains distributed by the fund

- AMIT cost-base adjustments

The important thing to understand is that the cash paid to you is not always the same as the taxable income attributed to you.

That is why the AMMA statement matters.

Why ATO pre-fill may not be the full picture

ATO pre-fill can be useful.

But it does not mean every ETF tax record has been handled for you.

One of the big traps with ETF tax is assuming that if the income appears in pre-fill, there is nothing else to track.

That may not be the case.

AMIT cost-base adjustments may appear on your AMMA statement, but they still need to be recorded against your investment records so your cost base is right when you eventually review a sale or CGT report.

This is where many ETF investors get caught.

The income side can look mostly handled.

The capital gains side may not become obvious until years later.

What is cost base?

Your cost base is broadly the tax cost of your investment.

For a simple ETF purchase, it usually starts with what you paid, plus relevant acquisition costs such as brokerage.

Starting cost base

This is the simple starting point. You buy 100 ETF units at $20 each.

For example:

You buy 100 ETF units at $20 each.

Your starting cost base is:

100 × $20 = $2,000

If you later sell those units for $3,000, your capital gain or loss is generally calculated by comparing your sale proceeds with your cost base.

In simple terms:

Sale proceeds minus cost base equals the capital gain or loss before other tax rules, and your personal position is considered.

But with ETFs, your cost base may not stay the same forever.

That is where AMIT cost-base adjustments come in.

What are AMIT cost-base adjustments?

Some ETF tax statements include amounts that increase or decrease your cost base.

These are often described using terms like:

- AMIT excess

- AMIT shortfall

- Cost base net amount

- Cost base increase

- Cost base decrease

The wording is not exactly friendly. But the idea is easier once you slow it down.

AMIT excess

Cost base decrease

An AMIT excess generally reduces your cost base. A lower cost base can mean a higher estimated capital gain when you sell later, before your personal tax position is considered.

AMIT shortfall

Cost base increase

An AMIT shortfall generally increases your cost base. A higher cost base can mean a lower estimated capital gain when you sell later, before your personal tax position is considered.

Do cost-base adjustments matter if you have not sold?

This was one of the webinar's biggest questions.

The practical answer is: they may not affect a CGT calculation until you sell, but they are much easier to track as you go.

If you have not sold any ETF units, you may not have a capital gains event for that holding in that year.

But that does not mean the annual cost-base adjustment is irrelevant.

It still affects the records you may need later.

The risk is leaving it for five or ten years, then needing to review a sale and realising you have years of AMMA statements, DRPs, ETF parcels and cost-base adjustments to rebuild.

That is when ETF tax can get painful.

It is much easier to keep the records tidy each year than to recreate everything later.

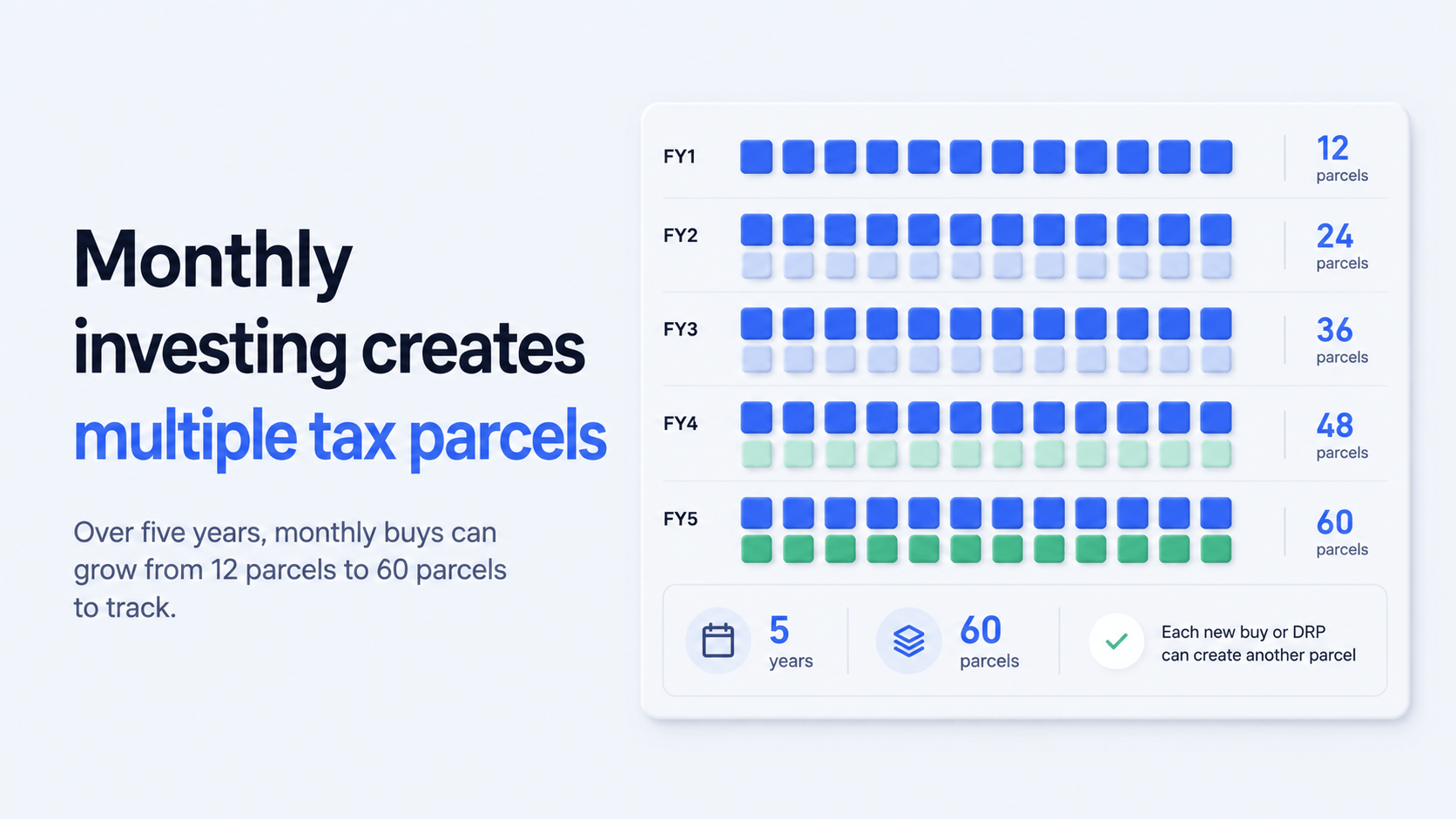

Why DCA and DRP make this harder

A parcel is a group of units bought at a particular time, at a particular price.

If you buy an ETF once, you have one parcel.

If you dollar-cost-average every month, you create a new parcel every month.

If you have DRP enabled, each dividend reinvestment can create another parcel.

Each parcel can have its own:

- purchase date

- number of units

- purchase price

- brokerage

- cost base

- AMIT adjustments over time

- CGT discount eligibility

Now imagine investing monthly for five years.

That can mean 60 separate parcels for one ETF.

If the ETF issues an AMMA statement each year with cost-base adjustments, those adjustments may need to be applied across the parcels you held during the relevant periods.

That is the part many investors underestimate.

It is not one ETF statement.

It is the record-keeping that builds up over years.

What happens when you sell?

When you sell ETF units, you generally need to work out the estimated capital gain or loss based on your records.

This is where parcel selection matters.

Say you bought the same ETF twice:

- Parcel A: 100 units at $10

- Parcel B: 100 units at $15

Later, you sell 100 units at $20.

You received $2,000 from the sale.

But which 100 units did you sell for CGT reporting purposes?

If you use the older parcel first, your cost base may be different from using the newer parcel first.

That can change the estimated capital gain for that financial year.

Common parcel-selection methods include:

- FIFO, first in, first out

- LIFO, last in, first out

- Max gain

- Min gain

- Min CGT

- Manual parcel selection

These methods are not recommendations. There are different ways to assign sold units to buy parcels for reporting purposes.

The important part is keeping clear records of which parcels were used.

If you sell some units this year, then sell more in five years, you need to know which parcels are still available. Otherwise, you risk double-counting or using units in your records that were already used in a previous CGT calculation.

Can you just pick one method and stick with it?

Some investors prefer the simplicity of using one method consistently.

That may make record-keeping easier.

But the key point is not just whether you call it FIFO, LIFO, min gain or manual selection.

The key is identifying and recording which parcels were used for each sale.

If you use a tool, spreadsheet or an accountant, the records need to show what happened.

Same investor. Same holding. Same sale price. Different parcel allocation. Different estimated gain.

That is why CGT reporting is not just about the sell trade.

It is about the history behind the sell trade.

What about US ETFs and foreign ETFs?

Australian-listed ETFs and US-listed ETFs can involve different tax records.

Australian ETFs may provide AMMA statements under the AMIT regime.

US-listed ETFs, such as US-domiciled funds, generally do not provide an Australian AMMA statement in the same way. Investors may need to consider foreign income, withholding tax, foreign income tax offsets, exchange rates and the timing of annual statements or broker reports.

This can get more complex if your broker reports income before final annual tax components are available.

If you hold US ETFs, foreign ETFs or investments across multiple brokers, it is worth keeping detailed records and speaking with a qualified tax professional about your circumstances.

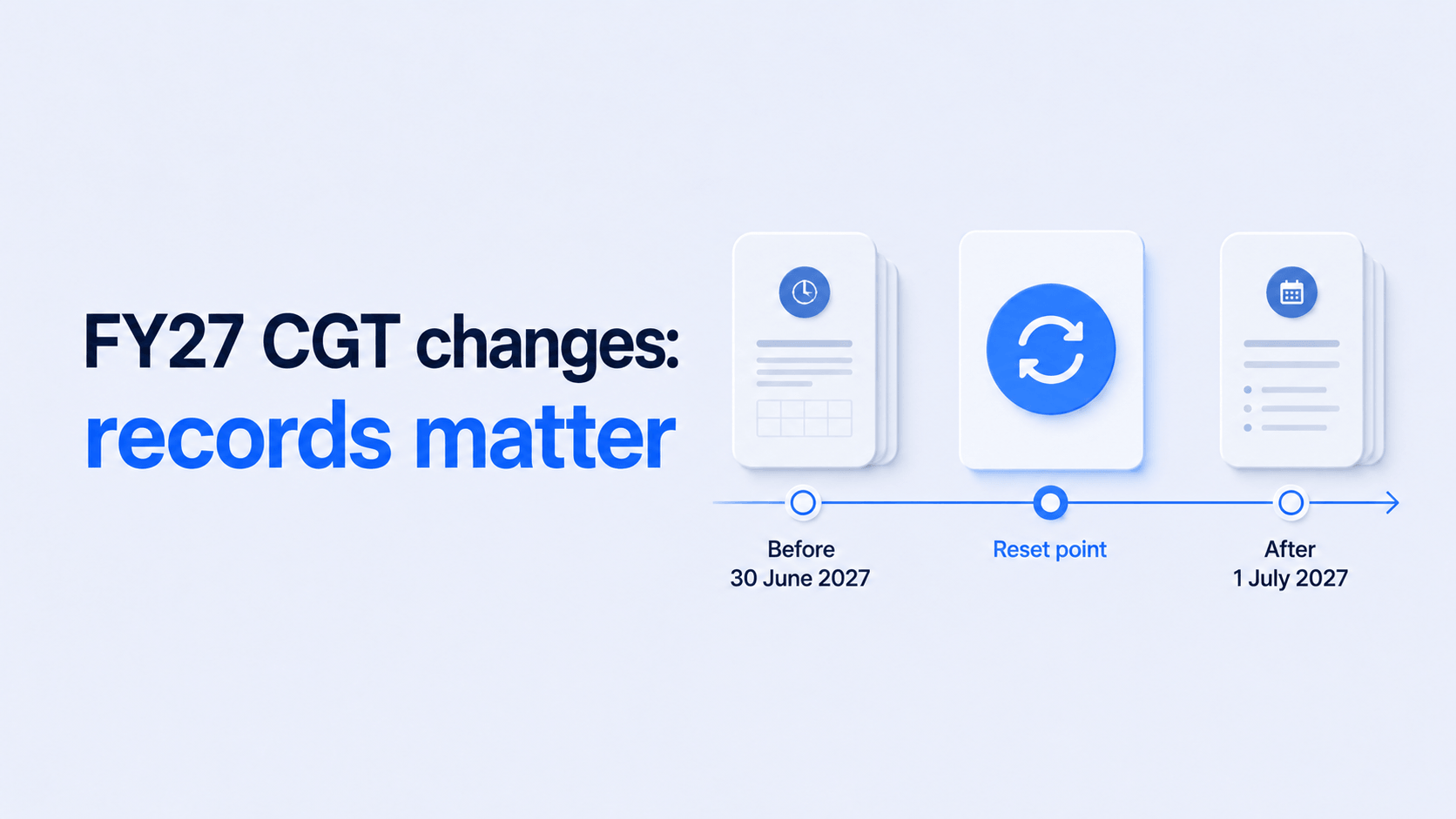

What about the CGT changes from FY27?

From 1 July 2027, CGT rules are changing.

The Australian Government Budget 2026-27 Tax Reform page states that the Government will replace the 50% Capital Gains Tax discount with an inflation-based discount and introduce a minimum 30% tax on gains from 1 July 2027.

The same Budget material states that the CGT reforms will only apply to gains arising after 1 July 2027.

Why parcel history may matter more

From 1 July 2027, CGT rules are changing. The practical takeaway for investors is to keep clean records of dates, parcels and cost-base adjustments.

This is an important topic, but it is also one where investors need to be careful.

The record-keeping point is simple:

These changes may make accurate parcel history, cost-base records and dates more important when reviewing future CGT reports.

In the webinar, we covered concepts such as:

- the current 50% CGT discount

- indexation from 1 July 2027

- the market value reset point

- how existing parcels may straddle two systems

- why parcel history may still matter after the change

This does not mean you need to buy, sell, hold, switch or restructure based on this article.

Those decisions depend on your personal circumstances.

But from a record-keeping perspective, the message is clear: the more complete your parcel history is, the easier it may be to review future CGT reports and scenario estimates.

Common ETF records to keep at tax time

Common records that may be useful for ETF tax reporting include:

- AMMA statements for each ETF you hold.

- Income components, including franking credits, foreign income and tax offsets.

- AMIT cost-base increases or decreases.

- Buy, sell and DRP records.

- Past disposals and the parcels used for each sale.

- Source documents, even if you use software or an accountant.

- Reports to review with your accountant or registered tax agent before lodging.

You do not need to become a tax expert.

But you do need records that can be checked.

That is the main thing.

How Navexa helps

Navexa is built to help investors track their portfolio data in one place.

That includes performance, income, trades, parcels, CGT reporting and taxable income reporting.

For ETF investors, Navexa can help by:

- importing trade history from supported brokers

- tracking buy and sell parcels

- recording DRPs

- helping apply AMIT cost-base adjustments

- comparing estimated CGT outcomes under selected parcel methods, based on recorded portfolio data

- keeping a record of prior disposals

- producing tax reports that can be reviewed with your accountant or registered tax agent

Navexa does not tell you what to buy, sell or hold.

It does not provide personal financial or tax advice.

What it does is help you organise the data, compare scenario estimates and prepare clearer reports based on the information recorded in your account.

That can make the conversation with your accountant easier, especially if you have been investing for several years, using DRP, dollar cost averaging, or investing across multiple brokers.

Using Pearler with Navexa

If you already use Pearler, Navexa’s integration can help bring supported trade data into your Navexa account.

This may reduce the manual work of building your portfolio history, especially if you invest regularly and want your portfolio records in one place.

Eligible Pearler users can access a Navexa discount here:

View the Navexa discount for Pearler users

Navexa is a portfolio-tracking and tax-reporting platform. Navexa does not recommend Pearler, any broker, any financial product or any investment strategy.

You can also download the webinar slides here:

Frequently asked questions

Do I need an AMMA statement if I have not sold any ETFs?

You may not need to calculate a CGT event for that ETF if you have not sold units, but the AMMA statement can still include income components and cost-base adjustments.

Those cost-base adjustments may affect your future CGT calculation, so keeping the statement and recording the adjustment can be useful.

Is the cash distribution the taxable income?

Not always.

The cash paid to you may not match the taxable income attributed to you by the ETF. The AMMA statement breaks down the tax components.

What is an AMIT cost-base adjustment?

It is an amount from the AMMA statement that may increase or decrease your cost base.

This matters because your cost base is used when calculating estimated capital gains or losses later.

Does an AMIT excess increase or decrease cost base?

In simple terms, an AMIT excess generally decreases your cost base.

A lower cost base can mean a higher estimated capital gain when you eventually sell, before your personal tax position is considered.

Does an AMIT shortfall increase or decrease cost base?

In simple terms, an AMIT shortfall generally increases your cost base.

A higher cost base can mean a lower estimated capital gain when you eventually sell, before your personal tax position is considered.

Can I use FIFO, LIFO or manual parcel selection?

Different parcel-selection methods can be used to allocate sold units to buy parcels.

The important thing is keeping accurate records of which parcels were used.

Navexa can help compare estimated outcomes under selected parcel methods, based on recorded portfolio data. It does not tell you which method is right for your circumstances.

Do US ETFs have AMMA statements?

US-listed ETFs generally do not provide Australian AMMA statements in the same way as Australian managed funds or ETFs may.

Foreign investments can involve various reporting issues, including foreign income, withholding taxes, foreign tax credits, and exchange rates. Speak with a qualified tax professional about your circumstances.

Does Navexa replace an accountant?

No.

Navexa helps track and report portfolio data. It does not replace personalised advice from an accountant, registered tax agent, financial adviser or legal professional.

Watch the full webinar

If you want the full walk-through, examples and discussion, you can watch the webinar replay here:

You can also download the slides here:

Final thought

ETF tax is not impossible.

But it does reward good records.

The earlier you understand your AMMA statements, cost-base adjustments, parcels, DRPs and CGT methods, the easier it may be to keep your portfolio records organised.

Navexa helps Australian investors track portfolio data, tax reports, income, parcels and CGT records in one place.

If you already use Pearler and want to see the Navexa discount for Pearler users, you can start here:

View the Navexa discount for Pearler users

Navexa is a portfolio-tracking and tax-reporting platform. Navexa does not recommend Pearler, any broker, any financial product or any investment strategy.

Disclaimer: This article is general information only and does not constitute financial, legal or tax advice. It does not take into account your personal circumstances, objectives or needs. Navexa provides portfolio-tracking and tax-reporting tools based on data recorded in your account, but does not provide personal financial, legal, or tax advice. Tax rules, platform features and legislation may change. Always speak with a qualified accountant, registered tax agent, financial adviser or legal professional before making financial, legal or tax decisions.